Bubbles and crashes [#25]

That was the subject line in a Monday afternoon email, from someone I’ve been working pretty closely with over the last year. The message was short:

“I’m getting more worried about an inevitable correction sometime soon. Wondering if we should pull out -- just till the market settles down.”

I can hardly blame her, she was being assaulted by the same headlines as the rest of us – the ceasefire in the Middle East had come apart again overnight, the price of oil had skyrocketed once more, and the share market had spent the morning giving back weeks of gains.

The entirely understandable response is to get out of the pot before this simmer boils over.

Have The Rules Have Changed (Again)?

Moments like these – drama, crisis, uncertainty – appear from time to time, at least somewhere in the world, and sometimes everywhere. It’s entirely natural to wonder whether the rules have changed this time. For those of my vintage, here are some that you’ll probably remember very well; at the time it was pretty easy to conclude that the rules of yesterday no longer apply today …

· The oil crisis of the early seventies convinced people that growth itself might be gone forever. A brand new word, ‘stagflation’, suddenly became very popular.

· Y2K was another new word that had us all spooked about a corporate apocalypse. On the evening of 31 December 1999 many sat up until well after midnight, waiting to see if everything would just turn off. The landmark film Fight Club was released just prior and took full advantage of the paranoia at the time. The counterpoint was the chorus of Prince’s song ‘party like it’s 1999’.

· When the GFC broke, a few years afterward, people were convinced the system itself was rotten underneath.

· And, a decade later, Covid convinced people that commerce could simply stop.

Each significant drama, at the time, felt like a sign of the end of the old world. Each one had smart, careful people utterly convinced that this time, the rules were changing forever.

And now we’ve got a ceasefire falling apart in real time, oil climbing by the day, and — as if that weren’t enough — an AI wildcard sitting off to the side, promising to either save the economy or upend it, depending which morning’s headline you happen to read.

The sun still rises

These events were all significant, for sure. And let’s not trivialise the knock-on effects, either. But underneath every one of those headlines there’s something we need to remember: people still need to eat. They need somewhere to live, a job to go to, medicine when they’re sick, an education for their kids, clothes on their back — and a way to pay for all of it.

That engine – supply meeting the basic reality of human demand – never stopped. Not once. Not in the seventies, not in 2000, not in 2008, not in 2020, and it will not stop in spite of today’s crisis either.

The engine keeps running. But there is something that does change, though, and that’s the story wrapped around the engine.

So – no – I don’t think it’s different just this time. For sure the content changes every time. But the context – supply and demand – hasn’t changed.

Which begs the question.

Does that mean the answer to the question ‘Should I pull out till this blows over?’ is always an automatic ‘No!’?

Why TimING isn’t as important as Time IN

Selling up “till this blows over” isn’t one decision. It’s two. You have to be right about when to get out — and right about when to get back in. Missing on either half of that trade is enough to cost you badly.

So – yes, absolutely: if you could successfully side-step the seemingly inevitable correction then it’d be a smart thing to do.

But!

The practical reality is that you can’t just get back in when stability seems to have been restored. For it to be a profitable exercise you need to get out and back in just at precisely the right time You only have to miss out by a teeny weeny margin to make it the wrong thing to do.

What’s this actually mean?

Every year new, peer-reviewed academic research adds to the already deep database of evidence that shows beyond a shadow of a doubt that the average investor earns meaningfully less than the very fund they’re invested in, purely because of when they buy in, sell out, and buy back in (if they do). They’re not getting in and out because the investment is dodgy or the market in which it’s deployed is dysfunctional, but because the investor buys when things feel safe and sells when things feel dangerous, which is almost exactly backwards.

Don’t take my word for it. Google it. Morningstar’s Mind the Gap research is one of the more defensible pieces of evidence in this space. There’s loads of other research, though.

And here’s why it’s backwards.

Look at any decade of market history and you’ll find that a small handful of trading days contributed a large chunk of the total return earned during the period. Hair-raising observations are revealed when you look at the raw data:

· Roughly speaking, in the last hundred years there have been about 30 corrections (or ‘crashes’, depending on your terminology) … but also 30 recoveries (or ‘booms’). The average loss during a correction has been 35%, and the average gain during a recovery 112%.

· Many of a decade’s best daily returns have occurred within a week or two of the worst ones. Miss just a handful of those superlative days and you’re handing back maybe half of the growth that entire decade delivered.

· Most recoveries emerge, without warning, from the smouldering wreck of a correction. In fact, in the last two decades about 40% of the S&P500’s best days occurred during a period of correction.

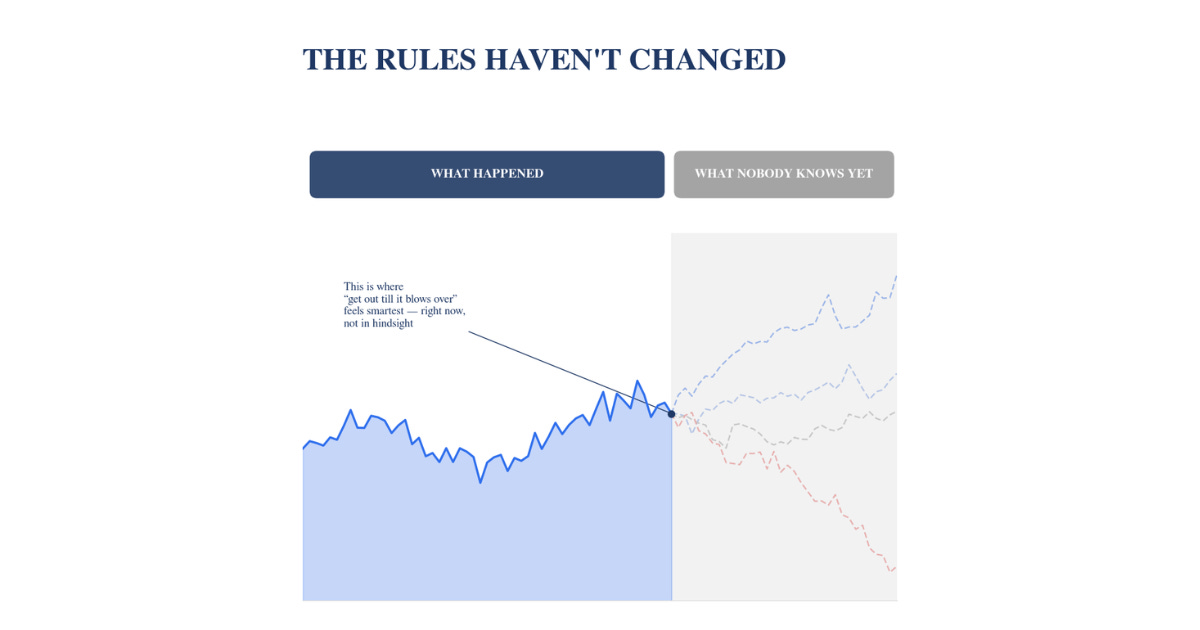

Recoveries don’t reveal themselves once the coast looks clear. They arrive while the coast still looks like a war zone, which is exactly when the “get me out till this blows over” instinct is loudest, and exactly when acting on it costs the most.

The keel below the waterline

So what do you actually do when faced with events like the ones we’re facing right now?

I certainly don’t subscribe to blindly declaring ‘stay calm, all is well’. A smile makes a lousy umbrella.

However – whereas some strategies are founded on the principles I’ve alluded to in this article, others are not. And if you’re not absolutely certain about the principles by which yours is constructed then you’ve got some urgent work to do.

Is your portfolio built in the hope that weeks like the ones we’re having these days would never come? Or was it built with the expectation that it would? I’m talking about the whole strategy, not just the investments you’ve picked, that’s just tickets to the dance.

The management rules which govern the overarching allocation of those assets, how and when it’s reassessed, your cash buffer, the order in which things get sold if income is needed. These rules need to be set up back when the seas are calm, precisely so that when the storm surge swells, it doesn’t force a decision made out of fear.

To extend this seafaring metaphor: that’s the whole point of a ship’s keel. It doesn’t seem to do anything dramatic and you can’t see it from the deck. It just sits below the waterline, doing the unglamorous job it was built for, whether the sea is flat or furious.

Best regards

Daniel Brammall

Two ways I can help:

1) Roadmap Experience (Advisory)

Leave with clearer next steps and a practical path forward.

Book your call → danielbrammall.com/roadmap-experience

2) Retirement Resilience Forecaster (DIY)

See best case, worst case, and what’s more likely, not a straight-line guess.

Get the Forecaster ($27 AUD) → danielbrammall.com/retirement-resilience-forecaster

This article is general information only and does not take into account your personal objectives, financial situation, or needs. It is not intended as personal financial advice and should not be relied upon as such. Before acting on any information, consider its appropriateness to your circumstances and seek professional advice tailored to your situation.