The gamble disguised as a retirement plan [#20]

“Will I have enough — no matter what?”

That simple retirement question can also show up as:

How much can I spend without running out?

Am I certain this can be my last paycheque?

What if the market crashes the day after I retire?

AI is transforming most industries and retirement planning is next — and the tools it’s bringing with it change your outlook entirely.

Rely on old thinking, though, leaving these questions unanswered, will continue to cost you resources you can’t get back. Like the time you spend trying to figure all this out. Like the opportunities that passed you by or even costly mistakes that crept in.

And in the background there’s that growing feeling this is still unresolved. It nags and gnaws. For some this is a persistent, low-grade, nuisance that is going to have to be dealt with sooner or later. For others it appears at 3am and feels a bit more like dread.

To properly understand how to resolve this dilemma let’s unpack how the current, popular solution falls well short.

How ‘Retirement 2.0’ answers it

The approach that still dominates retirement planning — what we’ll call Retirement 2.0 — goes something like this.

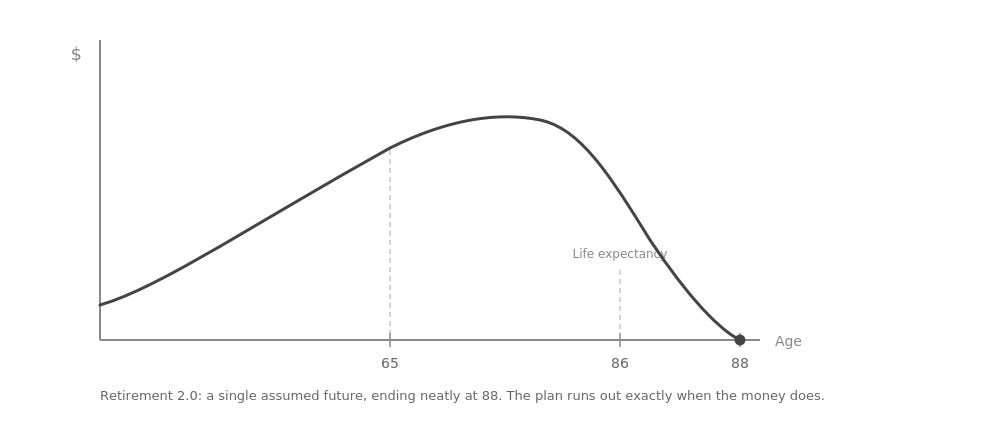

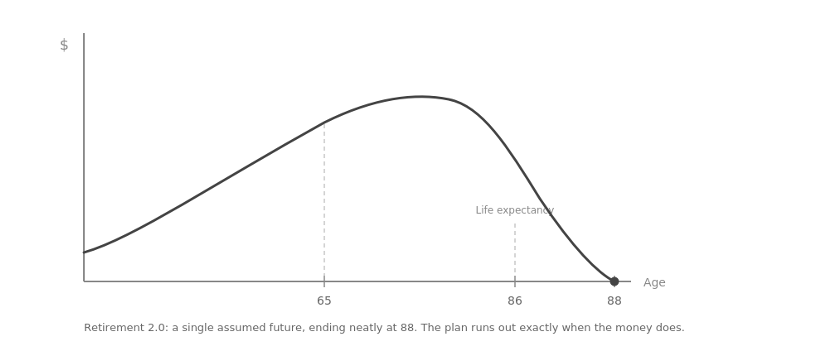

You want your nest egg to pay out an inflation-proof $100,000 a year across the life of your plan — scaling back to perhaps half or two-thirds of that in the final ten years, when the expectation is that life has slowed down considerably. Less travel. Less independence. More Netflix. It’s not a pleasant decade but at least it won’t cost much.

To see how that will work, you need to make some assumptions.

Over the last forty-plus years, the market has returned an average of around 10% (say) per annum. So we’ll use that as our baseline. Also, your life expectancy right now — let’s say 86 — is your target date.

If the money, earning that return, outlasts that age, happy days.

Run the forecast. The money lasts to age 88. The line slopes the right way. Sounds like a plan.

Take a fresh look at that exercise, though, and see what it’s actually asking you to believe. This is a ‘straight-line forecast’ and what it’s really saying is:

“If my portfolio earns this return, and I live about this long, then I should be fine.”

Notice how many ‘ifs’ have to work just right for you to be in the clear.

The return has to cooperate. The timeline has to cooperate. Life itself has to cooperate. Three big assumptions — and you need all three to play out more or less as expected before you can say with any confidence: “I’ll be fine”.

Phrased that way, the gaps are obvious. But this isn’t fringe thinking or outdated practice. Here’s what is still being published in 2026:

“Multiply your retirement spending number by 20. The rule of 20x is based on you earning a long-term average return on your retirement savings of 7 to 8 per cent, a fairly common long-term number for most balanced super funds.”

That perfect forecast looks like this:

When the bet doesn’t pay off

Bets feel fine when they’re going your way. The problem arrives when they’re not — and the problem with this particular bet is that you may not know you’re on the wrong side of it until it’s too late to do anything about it.

What does a straight-line forecast completely overlook?

If your portfolio takes a serious hit in the first few years of retirement — not a disaster, just a bad run at the wrong time — the mathematics of recovery become brutal. You’re drawing down on a smaller base, the compound growth that was supposed to carry you forward has been interrupted, and the plan that looked fine at 62 starts to look fragile at 70. Economists call this ‘sequence risk’ and it can happen anytime to anyone.

Next, the life expectancy figure baked into your straight-line plan is a population average. This means exactly half the people will live longer than that age. And here’s a subtlety that most plans miss entirely: life expectancy isn’t fixed. It climbs as you age. The person who makes it to 80 has a longer remaining life expectancy than the 60-year-old who was told to plan to 86. The target keeps moving but the plan doesn’t move with it.

Neither of these is a catastrophe. Neither requires a market crash or a medical emergency. They’re just what happens when a plan built for average conditions meets a life that isn’t average.

The discovery arrives with a sudden shock. Now you’re spooked and living smaller than you expected, pulling back on things you assumed were within reach, making compromises you didn’t plan to make. Or you’re taking very uncomfortable risks because the alternative is to run out of funds altogether.

It’s that 3am moment. A feeling this plan might actually have been a bet, and the window to do anything about it has already closed.

Retirement 2.0’s answer to the most important financial question of your life amounts to a leap of faith — and in the world you and I are ageing into, that’s not a plan, it’s a bet gone bad.

Retirement 3.0: replacing the bet with a confidence statement

Full Spectrum Forecasting starts with the same question — will I have enough, no matter what? — but refuses to answer it with a single assumed future.

Start with longevity. Your statistical life expectancy might be 86. But we know that half the people at your age will live beyond that, and that the figure keeps climbing as you get older. We also know that medical and technological advances are extending not just lifespan but healthspan — the quality of life within those extra years. Sure, it’s simple and tempting to assume your final decade will be a quiet, low-spending Netflix existence, but in the face of the mounting evidence to the contrary, this is increasingly hard to justify. Vibrant, active, engaged lives well into the nineties are no longer the exception. Planning for your last ten years to be miserable is a form of sour optimism that works against you.

So we extend the horizon. We plan to age 95, or beyond. We account for the strong possibility — not the certainty, but the realistic possibility — that you might be an accidental centenarian.

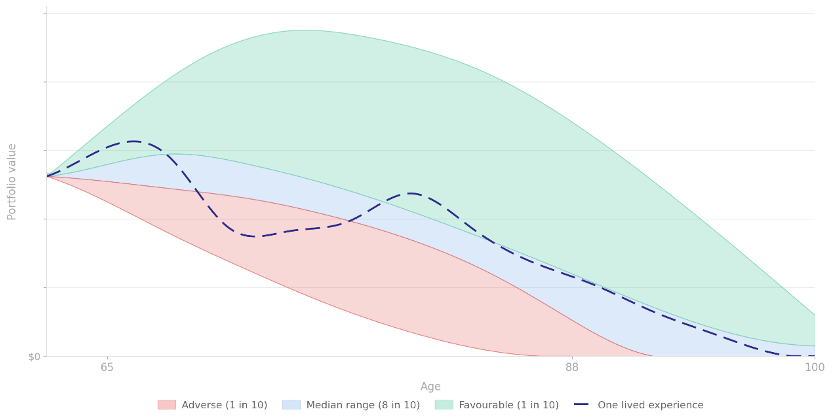

Now for the returns. Rather than pretending the market earns its forty-year average of 10% per annum every year of your plan, we model what actually happens if all market conditions occur.

Thousands of scenarios that include the good years and the bad ones. The sequences that begin well and turn south. The sequences that begin poorly but recover unexpectedly. Prolonged plateaus, sharp corrections. Every combination that history and probability can generate. With Ai, this is very doable.

What you get is not one line on a chart. You get a rich range of outcomes — wide at first, narrowing as the scenarios play out — showing you what might happen across the full spectrum of possibilities, including the most likely ones.

It looks like this:

Notice the bottom band. That represents the worst 10% of all scenarios modelled — the outcomes that occurred when things went badly: poor sequences, sustained market weakness, higher spending than anticipated, projected on top of a longer life than planned for.

If your money outlasts even those scenarios — if the line stays above zero even in the bottom band — then you can dispense with hope and instead make a confidence statement, something no straight-line forecast has ever been able to support:

I am 90% confident my money will not run out before I turn 88 — no matter what.

Those last three words are where the real value lives, here: ‘no matter what’ is not a wish or a bet-as-projection. It’s the result of having tested the plan against the bad scenarios, not just a single average one, and finding that it works 90% or more of the time. Or 95%. Or whatever level of certainty you want to aim for.

Ai didn’t invent this. It just made it yours

Full Spectrum Forecasting isn’t a new concept. Actuaries have been modelling probability distributions for decades. When it comes to retirement planning, though, the methodology hasn’t changed in 40 years. Apply that thinking to the world you and I are ageing into and you’ve got real trouble.

Compare the two.

Retirement 2.0 says: ‘If my portfolio earns its historical average and I live to roughly my life expectancy, I should have enough.’

Retirement 3.0 says: ‘I can be 90% confident my money will not run out — no matter what.’

The first statement is a bet. It will serve you well when conditions cooperate and leave you exposed when they don’t. At 3am, when life is shaping up to be anything but average, it has nothing to offer you — because it was never designed for that moment. It was designed for a spreadsheet.

The second statement is what a plan actually is. It was built for the bad scenarios, which means it can speak to them directly. When the market shocks occur without warning, when life throws curveballs, when your health lasts much longer than you expected — the answer is already in the plan. You’ve already tested it. You already know.

This is the difference between living on a prayer and knowing it’s already factored it in.

It’s also the difference between lying awake at 3am and going back to sleep.